Is Employer Health Insurance Enough in Abu Dhabi?

Healthcare in Abu Dhabi is improving, but family medical costs can still rise quickly. A simple doctor visit, specialist appointment, scan, dental issue, maternity need, or chronic condition can quickly show whether your employer's health insurance is truly enough. Many families assume that if insurance is provided by an employer, they are fully protected. That is not always the case.

For families, the real question is not only “Do we have insurance?” It is “Does this plan actually cover how our family uses healthcare?”

Current Landscape of Employer Health Insurance in Abu Dhabi

Health insurance is mandatory for Abu Dhabi residents. Under Abu Dhabi Health Insurance Law No. 23 of 2005, health insurance is compulsory for non-UAE nationals and their families living in the emirate. The law also states that employers must provide health insurance coverage for employees and their family members, including one wife and three children under 18. This makes Abu Dhabi different from Dubai, where employers mainly cover employees, and sponsors usually arrange dependent insurance separately.

A standard employer plan in Abu Dhabi may include:

Inpatient hospital treatment

Outpatient doctor visits

Emergency care

Some medicine coverage

Maternity benefits

Basic diagnostics

Access to selected clinics and hospitals

The problem is that “covered” does not always mean “fully covered.” Families still need to check limits, networks, co-payments, exclusions, and approval rules.

Why Modern Families Need More Than Basic Cover

Families today use healthcare differently. It is not only about emergencies. Parents may need pediatric care, maternity support, dental treatment, mental health support, optical care, vaccinations, chronic condition management, or regular specialist visits. Older dependents may need more frequent checkups and long-term medication.

Employer plans often work well for basic needs, but families may feel the gaps when they need:

Regular pediatric consultations

Dental braces or dental surgery

Glasses or eye tests

Therapy or mental health support

International treatment access

Better maternity hospital options

Ongoing chronic disease care

Faster specialist appointments

This is why employer health insurance may be enough for one family and weak for another.

The 2026 Outlook for Family Health Insurance

Families in Abu Dhabi should expect insurance needs to become more detailed, not simpler. Medical costs, digital health tools, remote consultations, preventive screening, and advanced diagnostics are changing how families use healthcare. UAE-wide health insurance requirements have also expanded, with the Ministry of Human Resources and Emiratisation noting that, from 1 January 2025, employers must purchase health insurance to issue or renew residency permits under the relevant scheme.

For families, this means annual policy reviews matter. A plan that worked two years ago may not fit your current medical needs, family size, or preferred hospitals.

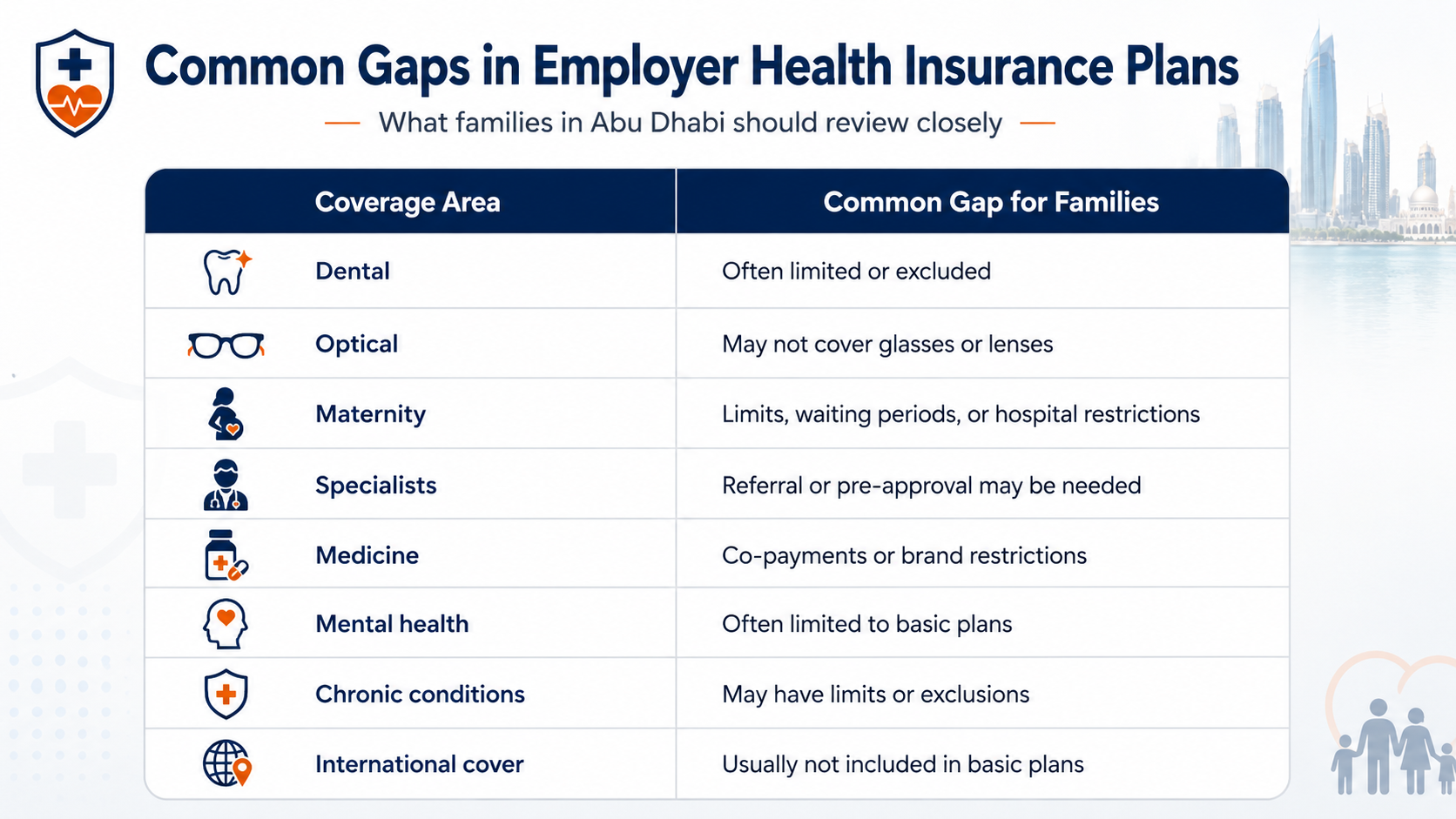

Common Gaps in Employer Health Insurance Plans

Employer insurance can be useful, but families should not assume that every medical need is well covered.

Coverage Area | Common Gap for Families |

Dental | Often limited or excluded |

Optical | May not cover glasses or lenses |

Maternity | Limits, waiting periods, or hospital restrictions |

Specialists | Referral or pre-approval may be needed |

Medicine | Co-payments or brand restrictions |

Mental health | Often limited to basic plans |

Chronic conditions | May have limits or exclusions |

International cover | Usually not included in basic plans |

The UAE government portal states that coverage level in Abu Dhabi can depend on salary, designation, and other factors. So two employees in the same city may not have the same quality of family cover.

When Employer Insurance May Be Enough

Employer health insurance may be enough if your family is generally healthy, uses in-network clinics, and has no major ongoing treatment needs. It may work well when:

Your preferred hospitals are in-network

Pediatric care is easy to access

Maternity cover fits your plans

Medicines are covered fairly

Specialist visits are not difficult

Co-payments are manageable

Emergency care is clear

Dependents are included properly

If all of these points check out, your employer plan may be sufficient.

When You Should Consider Extra Cover

You should consider private health insurance, a top-up plan, or supplementary cover if your employer plan feels restrictive. Extra cover may help if:

You want a wider hospital network

Your child needs regular specialist care

You are planning a pregnancy

You need dental or optical benefits

You travel often

You want international coverage

You have chronic conditions

You sponsor additional dependents

Your employer plan has low limits

Some families also look at separate individual plans for dependents if the employer’s family coverage is limited.

How Families Can Make a Better Decision

Start by reading the benefits table, not just the insurance card. Ask HR for:

Full policy benefits

Dependent coverage details

Network hospital list

Co-payment structure

Maternity terms

Dental and optical limits

Exclusion list

Pre-approval rules

Then compare that with your family’s real healthcare needs. A young couple without children may need a different plan from a family with two children, a pregnancy plan, and an elderly parent.

Conclusion

Employer health insurance in Abu Dhabi can be enough for some families, but it should never be accepted blindly. The plan may meet legal requirements, yet still fall short on dental, optical, maternity, specialist access, chronic care, international treatment, or hospital choice. Families need to review the actual benefits, not just confirm that a card exists.

Review your policy every year, confirm dependent coverage, check your hospital network, compare top-up options, and speak with an insurance advisor if your family has maternity, chronic care, dental, optical, or specialist needs.

Frequently Asked Questions

Is employer health insurance mandatory in Abu Dhabi?

Yes. Abu Dhabi law requires health insurance for non-UAE nationals and their families, and employers must provide coverage for employees and eligible family members.

Is employer health insurance mandatory in Abu Dhabi?

Yes. Abu Dhabi law requires health insurance for non-UAE nationals and their families, and employers must provide coverage for employees and eligible family members.

Does an Abu Dhabi employer have to cover my family?

Abu Dhabi rules require employers to cover employees and certain family members, including one wife and three children under 18. Extra dependents may need separate arrangements.

Is dental included in employer health insurance?

Not always. Dental is often limited, excluded, or added only in better plans. Families should check the benefits table.

Can I buy extra insurance if my employer plan is weak?

Yes. Many families consider top-up plans, private family insurance, or separate dependent cover when employer insurance is too basic.

Does an Abu Dhabi employer have to cover my family?

Abu Dhabi rules require employers to cover employees and certain family members, including one wife and three children under 18. Extra dependents may need separate arrangements.

Is dental included in employer health insurance?

Not always. Dental is often limited, excluded, or added only in better plans. Families should check the benefits table.

Can I buy extra insurance if my employer plan is weak?

Yes. Many families consider top-up plans, private family insurance, or separate dependent cover when employer insurance is too basic.

Related Posts

Abu Dhabi Insurance Checklist for Expats in 2026

What insurance do expats need in Abu Dhabi in 2026? Use this simple checklist to compare must-have, useful, and optional coverage before buying the right policy

Is Insurance in Abu Dhabi Worth It in 2026? Cost Guide

Is insurance in Abu Dhabi worth it in 2026? Compare real health and car insurance costs, legal rules, accident benefits, and hidden policy limits before you buy