Is Insurance in Abu Dhabi Worth It in 2026? Cost Guide

Insurance in Abu Dhabi is easy to see as just another yearly cost. You need it for health coverage, car registration, visa rules, and basic legal compliance. But the real question is different: does insurance actually give value, or are people only buying it because the law requires it?

In 2026, the answer depends on the policy. A weak plan may only keep you compliant. A good plan can protect you from hospital bills, accident repair costs, third-party claims, and sudden financial pressure.

What the Law Actually Requires in Abu Dhabi

Insurance is not optional in many everyday situations in Abu Dhabi. Health insurance is compulsory for non-UAE nationals and their families living in Abu Dhabi. The Abu Dhabi health insurance law also requires employers to provide coverage for employees, including the employee’s wife and three children under 18. Sponsors are responsible for the people they sponsor if those people are not covered by an employer. This means health insurance is not only a medical product. For many residents, it is also linked to employment, residency, and legal stay in the emirate.

Car insurance is also required if you own or drive a vehicle in the UAE. The Central Bank of the UAE explains that motor insurance mainly falls into two categories: third-party liability insurance and comprehensive insurance. Third-party insurance covers damage to others, while comprehensive insurance includes third-party coverage plus loss or damage protection for the insured vehicle, subject to policy terms.

What the law mainly expects

Valid health insurance for residents

Employer cover for eligible employees

Sponsor cover for dependents

Valid car insurance before registration

Third-party liability for drivers

Renewal before policy expiry

The law makes insurance necessary. The value comes from how useful the policy is when you actually need it.

Real Cost Breakdown

The real cost of insurance in Abu Dhabi is not only the premium. It also includes co-payments, deductibles, excluded treatments, repair limits, and rejected claims.

Health Insurance Yearly Cost in Abu Dhabi

TAMM lists the Abu Dhabi Basic Health Insurance Policy premium range from AED 750 to AED 18,072, depending on the case and policy details. TAMM also lists a fine of AED 300 per delayed month for late renewal.

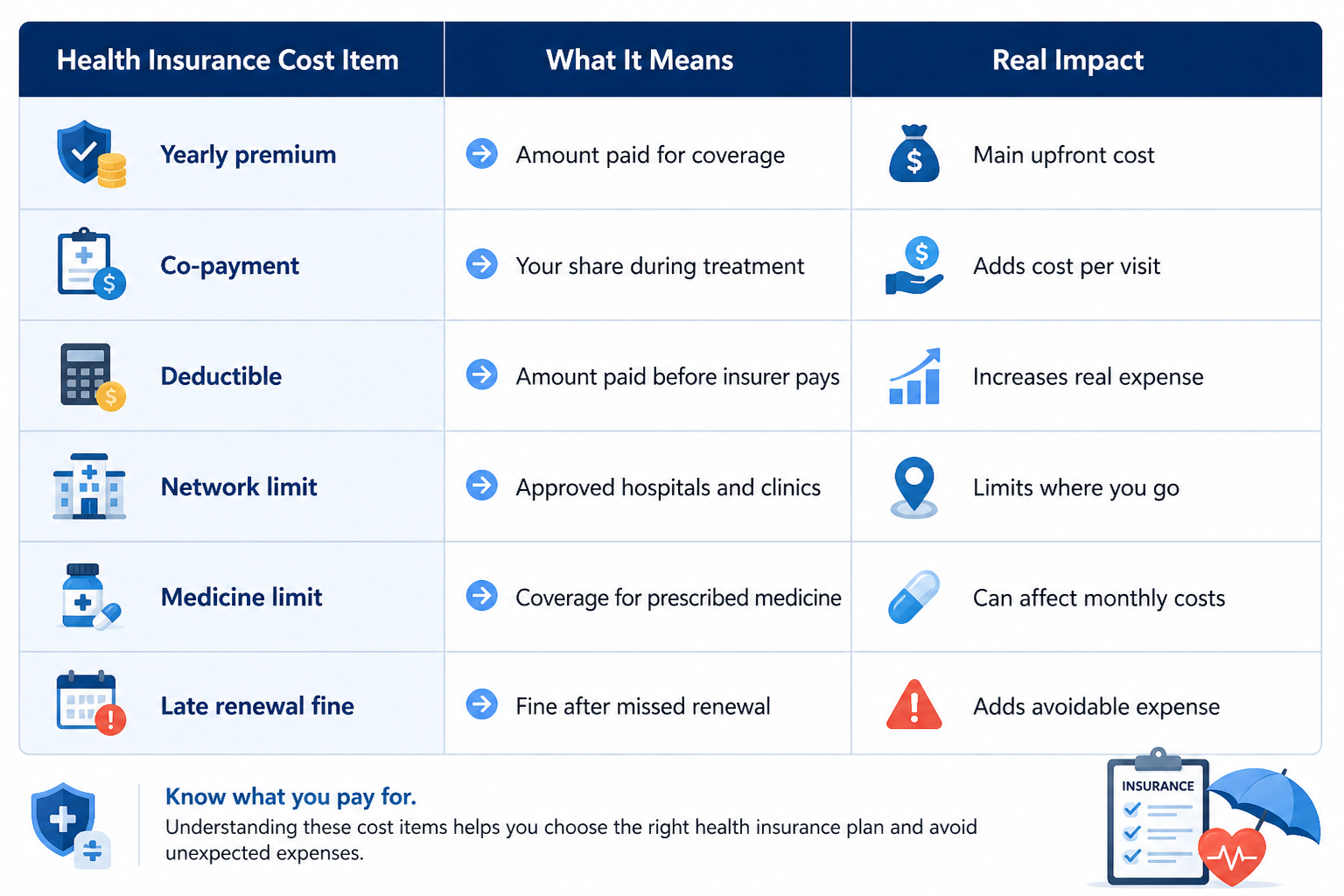

Health Insurance Cost Item | What It Means | Real Impact |

Yearly premium | Amount paid for coverage | Main upfront cost |

Co-payment | Your share during treatment | Adds cost per visit |

Deductible | Amount paid before insurer pays | Increases real expense |

Network limit | Approved hospitals and clinics | Limits where you go |

Medicine limit | Coverage for prescribed medicine | Can affect monthly costs |

Late renewal fine | Fine after missed renewal | Adds avoidable expense |

Car Insurance Average Premium in Abu Dhabi

Car insurance pricing changes based on car value, model, driver profile, claims history, and coverage type. A 2026 Abu Dhabi car insurance guide lists third-party liability premiums around AED 750 to AED 1,600 yearly, while comprehensive insurance often ranges from AED 1,300 to AED 4,500 or more.

A wider UAE 2026 estimate puts average annual car insurance at AED 1,200-AED 5,000, with comprehensive cover often priced as a percentage of the car’s value.

Car Insurance Type | Estimated Yearly Cost | Best Fit |

|---|---|---|

Third-party insurance | AED 750 to AED 1,600 | Older low-value cars |

Comprehensive insurance | AED 1,300 to AED 4,500+ | Newer daily-use cars |

Add-on coverage | Varies by insurer | Extra risk protection |

Real Benefit Scenarios

Insurance becomes easier to understand when you look at real situations.

Emergency Hospitalization

Imagine a resident needs sudden hospitalization after an accident, chest pain, infection, or a serious medical episode. Without proper health insurance, the cost can quickly become difficult to manage.

A useful health insurance plan may help with:

Emergency room access and treatment

Hospital admission and inpatient care

Doctor consultations during recovery

Approved medicines and tests

Lower out-of-pocket medical payments

Support during sudden health risks

The Basic Abu Dhabi Plan from Daman includes coverage for hospital stays, treatments, and medicines within Abu Dhabi, as well as emergency services within the UAE, subject to plan terms.

Accident Claims

For drivers, the benefit is clearer after an accident.

If you only have third-party insurance, your policy generally covers damage caused to other people, not damage to your own car. Comprehensive insurance can also protect your vehicle, depending on the policy terms. The UAE Central Bank explains that third-party liability is more affordable because it does not cover damage caused to the insured vehicle.

A useful car insurance policy may help with:

Third-party vehicle damage claims

Injury liability after accidents

Own car repair support

Agency or garage repair options

Roadside assistance is included

Lower stress after collisions

When Insurance Becomes Worth It

Insurance becomes worth it when it solves a real financial risk. That means the policy should help you avoid high, sudden costs, not just tick a compliance box. Good insurance gives value through:

Better access during emergencies

Lower sudden medical bills

Stronger protection after accidents

Less stress during claims

Better family financial safety

Stronger business risk control

More predictable yearly expenses

The best policy is not always the most expensive one. It is the one that matches your actual risk.

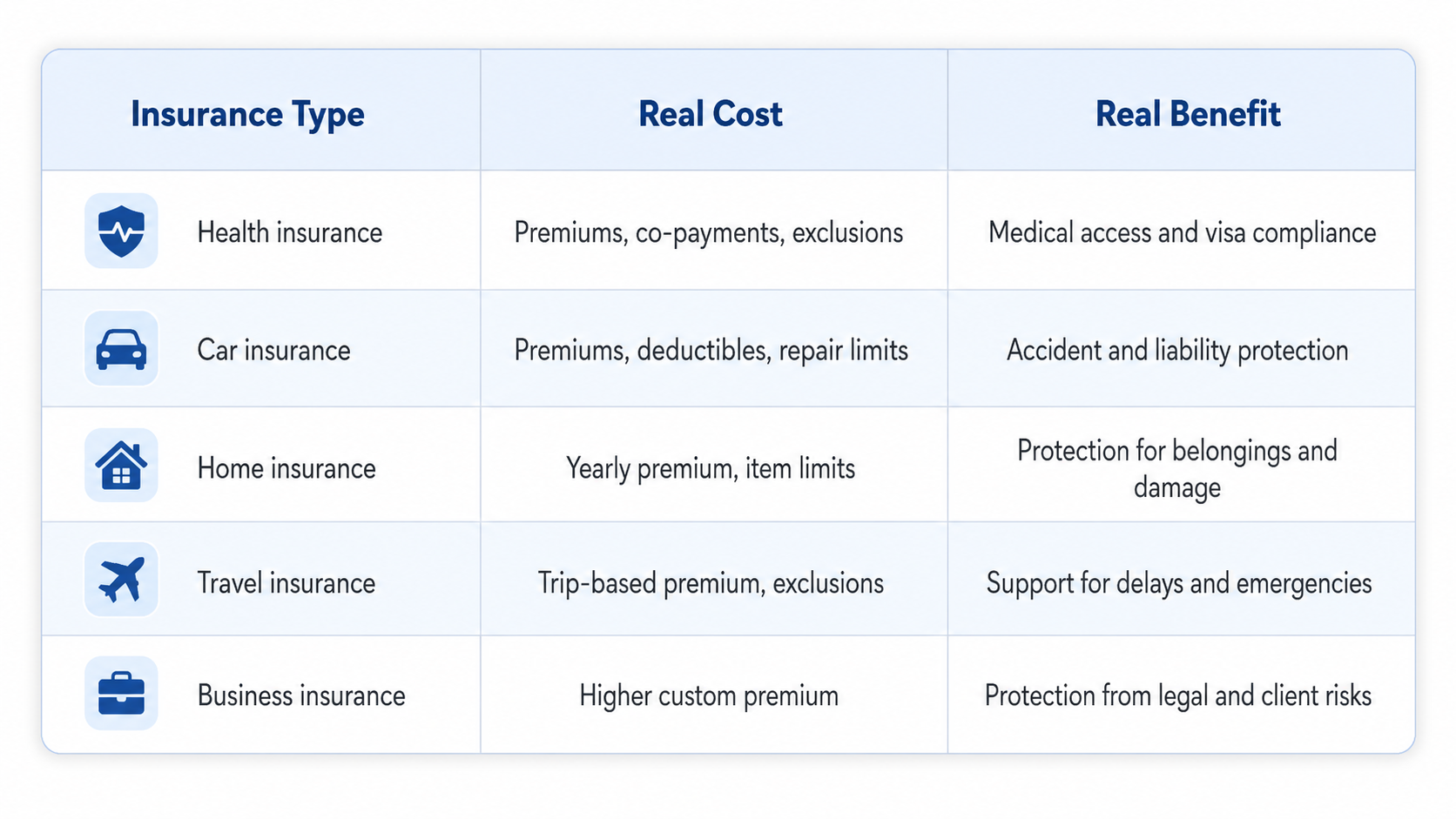

Real Costs vs Real Benefits

Use this table to compare the real cost and value of different insurance types in Abu Dhabi before choosing a policy.

Insurance Type | Real Cost | Real Benefit |

|---|---|---|

Health insurance | Premiums, co-payments, exclusions | Medical access and visa compliance |

Car insurance | Premiums, deductibles, repair limits | Accident and liability protection |

Home insurance | Yearly premium, item limits | Protection for belongings and damage |

Travel insurance | Trip-based premium, exclusions | Support for delays and emergencies |

Business insurance | Higher custom premium | Protection from legal and client risks |

The best insurance plan is not always the cheapest. It is the one that reduces your real financial risk when a claim happens.

Watch this health insurance guide for 2026 to understand real policy value, hidden costs, and coverage decisions before buying insurance in Abu Dhabi.

Final Verdict

Insurance in Abu Dhabi is not just a legal requirement in 2026. It can feel that way if you buy the cheapest plan without checking the real coverage. The better way to judge insurance is simple: ask what the policy will actually do when you need medical care, file an accident claim, repair your car, or protect your family from a large bill.

Frequently Asked Questions

Is insurance mandatory in Abu Dhabi?

Yes. Health insurance is mandatory for non-UAE nationals and their families living in Abu Dhabi. Car insurance is also required for vehicle owners and drivers in the UAE.

Who pays for health insurance in Abu Dhabi?

Employers must provide health insurance for employees and eligible family members, including the employee’s wife and three children under 18. Sponsors must cover people they sponsor if they are not covered by an employer.

How much does health insurance cost in Abu Dhabi?

TAMM lists Abu Dhabi Basic Health Insurance Policy premiums from AED 750 to AED 18,072, depending on eligibility and policy details.

How much does car insurance cost in Abu Dhabi?

A 2026 Abu Dhabi car insurance guide lists third-party insurance around AED 750 to AED 1,600 yearly, while comprehensive insurance often ranges from AED 1,300 to AED 4,500 or more.

Related Posts

Abu Dhabi Insurance Checklist for Expats in 2026

What insurance do expats need in Abu Dhabi in 2026? Use this simple checklist to compare must-have, useful, and optional coverage before buying the right policy

Is Employer Health Insurance Enough in Abu Dhabi?

Is employer health insurance enough for families in Abu Dhabi? Learn common gaps, family coverage limits, top-up options, and key checks.